A research-led analysis of the 182 largest Global Capability Centres in India — the mega-GCC tier that employs 80% of the country's GCC workforce and is reshaping global enterprise.

182

Mega-GCCs Studied

1.35M

Total GCC Workforce

~80%

of India's GCC Employees

16

Sectors Mapped

11

Parent Geographies

India's Global Capability Centre (GCC) ecosystem is one of the most consequential structural shifts in modern global enterprise. Over 2,100 GCCs currently operate in India, collectively employing more than 1.7 million people. But the popular narrative — of a broad, distributed offshore landscape — misses the actual structure of the market.

At Zyoin Group, we built a hand-curated dataset of the 182 largest GCCs in India, each with 1,000 or more India-based employees as of early 2026. We call this the mega-GCC tier. Together, these 182 entities employ approximately 1.35 million people — roughly 80% of India's total GCC workforce. The remaining 20% is dispersed across approximately 1,700 smaller captives.

What follows is what that data reveals — and why it should fundamentally change how talent providers, recruiters, policy makers, and corporate leaders think about the GCC market in India.

"The single most strategic line in the data is not where mega-GCCs are concentrated. It is how concentrated they are: 80% of GCC workforce in 10% of entities; 62% under one parent country; 76% in two cities."

80%

Power-Law Concentration

10% of GCCs employ 80% of the workforce. The top 30 entities alone account for 62% of the cohort.

40%

BFSI Sectoral Dominance

BFSI leads with 545,000 workers across 31 GCCs. Tech has the highest density at 11,200 employees per GCC.

62%

US Parent-Country Share

103 US-headquartered mega-GCCs employ 839,000 people — more than 5× the next country (UK).

76%

Two-City Concentration

Bengaluru (58%) and Hyderabad (18%) host 76% of all mega-GCC workforce. Concentration will deepen.

The 182 mega-GCCs represent under 10% of India's roughly 2,100 GCCs — yet they employ approximately 80% of the total GCC workforce. Within the cohort, the concentration deepens even further:

This is not a gradient distribution. This is a power-law concentration — the same structural pattern that defines the world's most winner-take-most markets. For recruiters and talent providers, this means that coverage models built on the top 50–75 mega-GCCs capture the vast majority of addressable GCC hiring opportunity. Broad horizontal approaches that chase the long tail typically misallocate effort and revenue.

The most sophisticated talent partners in the GCC space already operate concentrated key-account models. The rest are still catching up.

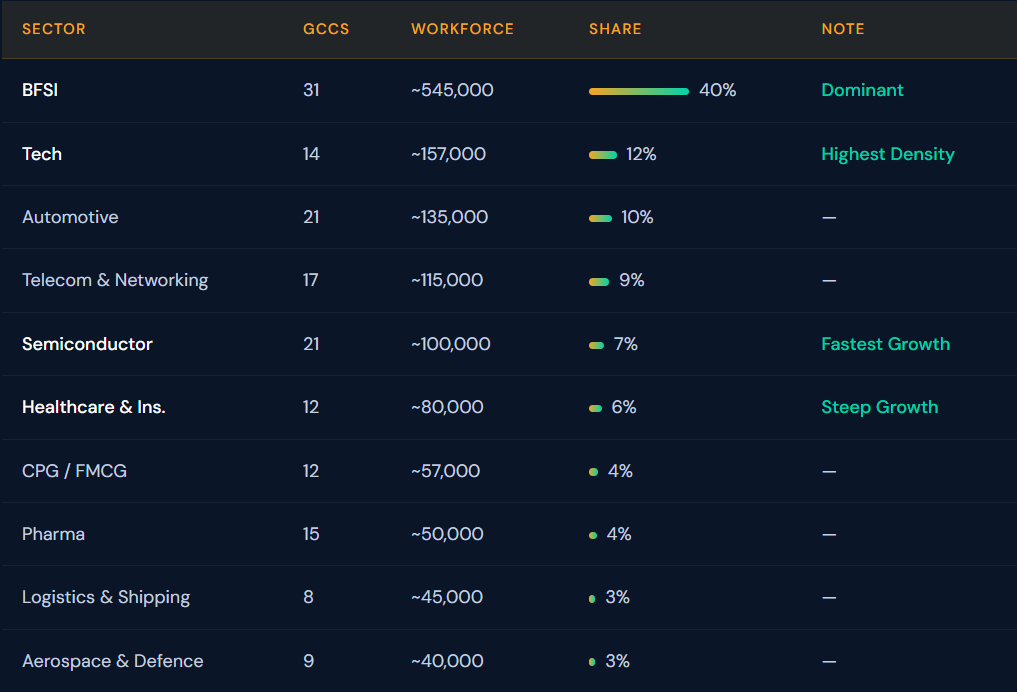

The 182 mega-GCCs span 16 sectors, with 12 sectors accounting for 95%+ of the cohort's workforce. Here's how the landscape breaks down:

BFSI is more category than sector. The 31 mega-GCCs in BFSI employ ~545,000 people. Wall Street and global UK banking clusters alone account for over 300,000 jobs. Breaking in is hard — expanding wallet share is the actual game for talent providers.

Tech is the highest-density sector. 14 mega-GCCs average 11,200 employees each — over 60% above BFSI's average. Tech captives have moved from shared services to global product engineering organisations. These are not back-office operations anymore.

Semiconductor and Healthcare are the steepest growth curves. The India Semiconductor Mission is supercharging the semiconductor cluster (21 mega-GCCs, ~100K employees). Healthcare is driven by US health-payer scaling at 20–25% CAGR. Both sectors will produce new Tier-1 anchor GCCs before 2028.

The Engineering R&D triad is high-specialisation, low-fungibility. Automotive, Telecom & Networking, and Aerospace & Defence require deep domain skills — ADAS, RAN/5G, DO-178C — that do not transfer across sectors. Talent strategy here is a fundamentally different problem.

CPG and Logistics are the under-discussed growth tier. Both scaled rapidly post-2017, led by GBS functions, with finance and supply chain anchoring and a growing digital and analytics layer now being added.

Layering parent-country data onto the sectoral view produces an even sharper concentration story. The US is not just the largest parent geography — it dominates to a degree that reshapes operational norms across the entire Indian GCC ecosystem.

103 US-headquartered mega-GCCs employ 839,200 workers — that's 62% of the mega-GCC cohort's total workforce, and more than 5× the workforce of UK-parented GCCs (~155,750).

This matters because country of origin shapes nearly every operational characteristic of an Indian GCC: working hours, compensation benchmarks, fiscal calendars, and senior-talent mobility patterns all anchor to US parent norms. The European tier (UK, Germany, Switzerland, Nordics — ~381K across 47 mega-GCCs) operates on slower decision cycles, longer-term partnerships, and comp packages anchored to predictability over peak.

For GCC recruitment and talent advisory firms, this concentration means that a single geographic expertise — the US parent playbook — is relevant to the majority of your addressable market.

The geographic concentration in the mega-GCC cohort is more extreme than most industry commentary acknowledges — and it is structural, not transitional.

Bengaluru's anchor status is unchallenged. It dominates every high-specialisation sector except pharma. Hyderabad is the credible #2 — and the only tier-1 city where new mega-GCC setups in the last three years have outpaced Bengaluru in count.

The tier-2 expansion narrative is real but not yet structurally significant. Successful tier-2 stories are all single-anchor-tenant captives driven by specific parent-company decisions, not broad market forces. Geographic concentration will deepen, not weaken — without a structural policy shift, Bengaluru–Hyderabad dominance is likely to increase over the next five years.

Within the 182 mega-GCCs, three distinct tiers emerge based on India headcount. Each exhibits different operational characteristics, strategic mandate, and market behaviour — which means talent strategy must be differentiated accordingly.

Tier 1

Anchors

38

10,000+ Employees · 63% of workforce

India is often the parent's largest global site. These entities drive parent-level transformation and set comp benchmarks that ripple across the ecosystem.

Tier 2

Scale-Ups

62

3,500–9,999 Employees · 25% of workforce

Have crossed the gravitational threshold (typically 2,000–3,000 employees), beyond which a captive moves from cost play to strategic capability node.

Tier 3

Builders

82

1,000–3,499 Employees · 12% of workforce

Most dynamic but also most fragile. Most were set up after 2017–18. The next 3 years will determine whether they cross the threshold or plateau as cost centres.

"There is a gravitational threshold around 2,000–3,000 employees. Below it, captives tend to remain cost centres. Above it, they begin reshaping the parent's global agenda."— Zyoin Group, The Mega GCCs of India

1. Don't treat GCC India as a distributed market

80% of the workforce sits in 10% of entities. Strategic actors — recruiters, service providers, policy makers — should build concentrated key-account models focused on the top 50–75 mega-GCCs, not horizontal reach across 2,100 GCCs.

2. The gravitational threshold is the central strategic line

Captives below 2,000–3,000 employees buy talent very differently from those above it. Tier-1 and Tier-2 captives engage through formal panels; Tier-3 captives engage through direct relationships. Strategy that conflates them underperforms.

3. Segment on three dimensions, not one

Sector alone is an incomplete lens. The full segmentation is sector × country × tier. A US Tier-1 BFSI captive, a German Tier-2 automotive captive, and a UK Tier-3 CPG captive run completely different operational motions — and need completely different talent strategies.

4. Assume geographic concentration deepens, not disperses

Workforce plans that assume broad tier-2 dispersal as a base case will overestimate capacity outside Bengaluru and Hyderabad. Tier-2 growth is real but anchor-tenant-driven, not market-driven — plan accordingly.

Three trajectories will define India's mega-GCC landscape over the next four years:

BFSI will continue to dominate by absolute scale, but growth rates will moderate. The Tier-1 BFSI cohort is approaching operational saturation in core hubs and will grow at single-digit rates while continuing to consume the largest share of senior talent supply.

The India Semiconductor Mission tailwind brings entirely new role types India has not hired at scale before. The US health-payer cluster is on track to scale at 20–25% CAGR for at least three more years. Both will produce new Tier-1 anchors by 2028 — creating meaningful new opportunity for specialised talent partners.

The long tail of Tier-3 builders will keep adding new entrants but at a more measured pace. Available leadership talent — not entry-level supply — will become the binding constraint. Many Tier-3 captives will not successfully cross the gravitational threshold and will plateau as cost centres.

India's mega-GCC ecosystem is no longer an offshore market. It is a concentrated, capability-led, structurally consequential layer of global enterprise — one that, in some functions, simply cannot be assembled at this scale anywhere else in the world.

The four structural facts — power-law concentration, BFSI dominance, US parent-country dominance, and Bengaluru–Hyderabad geographic concentration — are not new individually. But assembled, measured, and segmented at this resolution, they reframe the strategic conversation entirely.

At Zyoin Group, this research sits at the core of how we think about GCC talent acquisition, executive search, and staffing advisory. Understanding the structure of the market is the prerequisite for serving it well.

"India's mega-GCC ecosystem is no longer an offshore market. It is a concentrated, capability-led, structurally consequential layer of global enterprise, one that, in some functions, simply cannot be assembled at this scale anywhere else."

Whether you're scaling a Tier-1 anchor or crossing the gravitational threshold, Zyoin Group brings deep GCC market intelligence to your talent strategy.